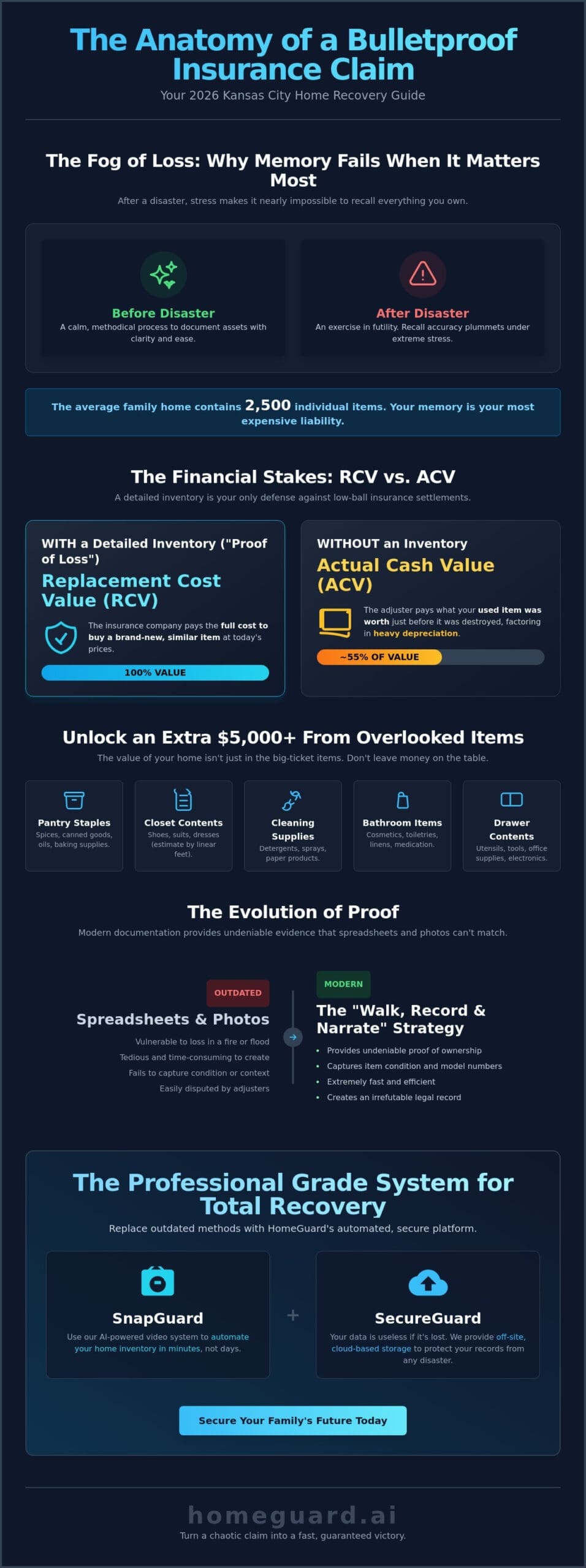

Your memory is your most expensive liability. After a disaster strikes Kansas City, the mental fog of loss makes it nearly impossible to recall the 2,500 average items scattered across a standard family home. You probably feel that your policy is a total safety net, yet without a verified household items list for insurance claims, that net has massive holes. It is a harsh reality that insurance adjusters often rely on your forgetfulness to minimize payouts. We know the stress of trying to prove what you owned while standing in the middle of the wreckage. It is overwhelming, frustrating, and entirely preventable.

This 2026 Kansas City Recovery Guide provides the structured, room by room checklist you need to ensure no asset is forgotten. You will learn how to secure the maximum payout by mastering the difference between Replacement Cost Value and Actual Cash Value. We will show you how to use SnapGuard to document assets in minutes and SecureGuard to protect that data. This article outlines a systematic path to total financial recovery. We are giving you the professional grade tools from HomeGuard to turn a chaotic claim into a fast, guaranteed victory for your family’s future.

Key Takeaways

- Identify why your inventory serves as a legal “Proof of Loss” document, providing your only defense against low-ball insurance settlements.

- Build a comprehensive household items list for insurance claims by documenting the “hidden” contents inside drawers and closets that most homeowners miss.

- Recover $5,000 or more in lost value by including often-overlooked items like pantry staples, cleaning supplies, and bathroom essentials.

- Transition from static photos to the “Walk, Record, and Narrate” video strategy to provide adjusters with undeniable proof of ownership.

- Replace outdated spreadsheets with the HomeGuard system, using SnapGuard to automate your recovery before the next storm hits.

Why a Detailed List of Household Items is Your Only Financial Defense

The contrast between “Before” and “After” is stark. Documenting your home today is a calm, methodical process. You can walk through your rooms, open drawers, and record details with ease. However, documenting a home after a total loss is an exercise in futility. Memory fails under pressure. Scientific studies on high-stress events show that recall accuracy drops significantly when cortisol levels spike. You won’t remember the brand of your toaster or the number of suits in your closet. You’ll only remember the big items, leaving thousands of dollars on the table.

The Financial Reality of Insurance Claims

Insurance adjusters use generic depreciation tables when specific item data is missing. If you claim “one television” without a model number or purchase date, they’ll pay the lowest possible value. You must understand the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV). RCV covers the cost to buy a brand-new version of your item at today’s prices. ACV only pays what your used item was worth the second before it was destroyed. Without a detailed list to prove your items’ quality, adjusters default to ACV. Providing a documented “Proof of Loss” is the homeowner’s primary legal burden to secure a full RCV payout.

Why Kansas City Homeowners Face Unique Risks

Kansas City residents live in a high-risk corridor for property damage. Between the violent spring tornado seasons and the flash flooding that plagues local basements, the threat to your physical assets is constant. A paper list kept in a filing cabinet offers zero protection against a 2026 storm surge or a fire. This is why a digital home inventory spreadsheet is the only logical choice for local families. Digital records, especially when backed up through SecureGuard, ensure your inventory is accessible from any phone or computer, even if your house is gone. At HomeGuard, we believe that off-site, cloud-based storage is not a luxury; it’s a necessity for Midwest survival.

Room-by-Room Breakdown: Essential Inventory for Every Home

Living Areas and Bedrooms

The Kitchen and Dining Room

The kitchen is arguably the most expensive room per square foot in a Kansas City home. Major appliances like your refrigerator, stove, and dishwasher represent thousands of dollars in potential loss. You should verify that you have model numbers for all these units. Use SecureGuard to store digital versions of your manuals and purchase receipts. This ensures that even if the physical appliance is destroyed, your proof of its value remains intact. Small appliances also add up quickly. High end espresso machines, blenders, and air fryers can easily total over $2,000 in a single room. Remember to open the cabinets to document your cookware, especially if you own premium brands like Le Creuset or fine china sets.

Basements, Garages, and Attics

These areas often become the “forgotten zones” during a claim. In Kansas City, basements are particularly vulnerable to flooding. Never just photograph a stack of storage bins. You must document the contents. A single bin labeled “Winter Gear” might contain four high end coats worth $300 each. In the garage, focus on the items that represent significant investment:

- Storage Bins: Open the lid and record what is inside, not just the box.

- Power Tools: Capture specific brands like DeWalt or Milwaukee.

- Sports Gear: List bicycles, camping equipment, and fitness machines.

Bicycles and fitness machines are high value items that are frequently under-claimed because owners forget they exist during the post disaster chaos. Following a structured inventory plan is the only way to ensure your garage and basement assets are fully protected from financial loss. Documenting these areas today is a simple way to secure your family’s future.

Beyond the Big Stuff: The Most Commonly Forgotten Items

Most homeowners focus on the big ticket items. They list the 75 inch TV, the leather sofa, and the stainless steel refrigerator. This is a mistake that costs thousands. The true value of your home is often hidden in plain sight. It’s buried in your cabinets, tucked into your linen closet, and lined up on your bathroom vanity. When building a household items list for insurance claims, you must account for the high volume of low cost items. Individually, a bottle of spice or a bath towel seems insignificant. Collectively, they represent a massive financial investment that insurance companies are happy to ignore if you don’t prove they existed.

In a total loss scenario, these “invisible” assets can easily exceed $5,000 in replacement value. If you forget to document them, you’re effectively giving that money back to the insurance company. Learning how to create a home inventory that includes these consumables is the difference between a partial recovery and a complete one. At HomeGuard, we see families lose significant sums because they didn’t think their “junk drawer” or “pantry” was worth the effort. It is.

The “Invisible” $5,000 in Your Cabinets

Think about your cleaning closet. You likely have a vacuum, a steam mop, and dozens of specialized detergents and chemicals. Replacing an entire household’s worth of cleaning supplies can cost $400 to $600 alone. Now, look at your pantry. A collection of high end spices, bulk grains, and organic oils can represent a $1,000 investment. Don’t forget your linens. High thread count sheets and plush towels are expensive. A single set of premium bedding can cost $200. When you multiply that by every bed in your home, the numbers become staggering. Use SnapGuard to quickly scan these areas. You don’t need to list every bottle. You just need to prove the volume and quality of what you owned.

Personal Care and Hobbies

The bathroom vanity is one of the most under documented areas in the house. Between electric toothbrushes, professional hair dryers, and luxury skincare, the contents of a master bathroom often exceed $2,500. Medicines and high end perfumes add even more value. For those who invest in premium lifestyle essentials from curated sources like Adamase, these items are essential for your daily life; you’ll have to buy them all again immediately after a disaster. Document them now so you aren’t paying out of pocket later.

Documenting for Proof: How to Prove Ownership Before Chaos

Static photographs are no longer the gold standard for insurance claims. While a picture shows an item exists, it rarely proves the specific quality or condition required for a full Replacement Cost Value payout. To build an airtight household items list for insurance claims, you must adopt a more dynamic strategy. You need a method that provides undeniable evidence before the stress of a disaster cloud your memory. Professional adjusters prioritize clear, timestamped evidence that leaves no room for interpretation or generic depreciation.

The most effective way to streamline this process is by using a specialized home inventory app. This technology replaces the slow, manual entry of spreadsheets with rapid visual capture. By moving through your home systematically, you create a digital witness that stands up to scrutiny. This is about financial self defense. You are not just taking a video; you are creating a legal record of your assets.

The SnapGuard Method: Walk, Record, Narrate

Speed and detail are the two pillars of the “Walk, Record, and Narrate” strategy. You don’t need to be a professional filmmaker to do this correctly. Start at your front door and move clockwise through every room. The key is to open every door and every drawer while the camera is rolling. Hidden items are the ones most frequently forgotten after a loss. As you move, narrate the details. Speak clearly about the brand, the age of the item, and the approximate cost.

Using SnapGuard allows for high speed video capture that adjusters trust because it provides a continuous, unedited look at your property. A narrated video acts as a timestamped witness to your belongings. If you show a 2024 Sony Bravia and state its purchase date, the adjuster cannot easily default to a generic “55 inch TV” valuation. This simple action can save you thousands of dollars in disputed value.

Securing Your Proof of Loss

High value items require a three pronged approach to evidence: the visual recording, the model number, and proof of purchase. We call this the “Receipt Rule.” If you have lost the physical receipt, don’t panic. A photo of the owner’s manual or the serial number plate on the back of an appliance often serves as sufficient proof of ownership. However, where you store this data is just as important as how you record it.

Local storage is a single point of failure. If your phone is destroyed in the same 2026 Kansas City storm that takes your home, your inventory is gone. You must use cloud redundancy to protect your data. At HomeGuard, we provide the infrastructure to ensure your records are accessible from any device, anywhere. Once your inventory is finished, upload it to SecureGuard immediately. This ensures your proof is locked away and ready the moment you need to file a claim with ClaimGuard. Protect your investment by documenting it today.

Moving Beyond Spreadsheets: Automating Your Inventory with HomeGuard

Manual spreadsheets are where recovery efforts go to die. They are tedious, time-consuming, and far too easy to abandon before the job is finished. For the modern Kansas City family, the “old way” of documenting property is a liability. You don’t have forty hours to type every item into a cell. You need a system that works as fast as your life does. HomeGuard was built on a “survivor-led” philosophy by experts who navigated the wreckage of real disasters. We saw how memory failed and how insurance companies used that failure to save money. We built this ecosystem to ensure that never happens to you.

This commitment to data-driven recovery extends to the professional sector as well; agencies that serve restoration and HVAC companies often utilize LeadOpsIQ to ensure they can provide timely assistance to families and businesses in the wake of a disaster.

A comprehensive household items list for insurance claims shouldn’t be a chore that lasts for weeks. It should be a professional grade asset that you can generate in a single afternoon. By shifting from manual entry to automated capture, you remove the human error that leads to thousands of dollars in lost payouts. This isn’t just about organization; it’s about financial self-defense. It’s about making sure that when a 2026 storm hits, you’re the most prepared person in the room. Stop procrastinating and protect your assets today.

The HomeGuard Ecosystem

Our system is designed with a three pillar approach to total recovery. Each tool serves a specific purpose in the timeline of a disaster, moving you from preparation to payout without the typical stress. This synergy ensures you never leave money on the table.

- SnapGuard: This is your high speed entry point. You can document an entire four bedroom home in under an hour. Just walk, record, and narrate.

- SecureGuard: This is your vault. We provide lifetime cloud access for your property records, ensuring your evidence is safe even if your physical hardware is destroyed.

- ClaimGuard: This is your advocate. When it’s time to face the insurance company, we provide the expert guidance needed to file your household items list for insurance claims with total confidence.

Next Steps for Kansas City Homeowners

Preparation is a binary choice. You’re either ready, or you aren’t. To get started, download the HomeGuard Complete kit and choose a date this weekend. We recommend scheduling a “Documentation Day” once a year to keep your inventory current. As you buy new electronics, furniture, or appliances, take sixty seconds to record them. This small habit prevents the “memory gap” that adjusters rely on. Don’t wait for the sirens to sound. Protect What You Own. Recover What You Lose.

Take Control of Your Financial Future

HomeGuard was founded by a fire survivor who used these precise strategies to recover 100% of their claim value. We designed this system for Kansas City homeowners who value speed and security over tedious manual entry. There are no complex spreadsheets required. By using SnapGuard and SecureGuard, you replace chaos with a structured, cloud-protected record of your life’s work. Don’t wait for a 2026 storm to prove that you weren’t ready. The difference between a partial payout and a total recovery is the action you take while your home is still standing.

Protect Your Assets Now: Get the HomeGuard Inventory System

Frequently Asked Questions

Is a video inventory better than a written list for insurance claims?

Yes; video provides visual context and proof of condition that a static list cannot match. It captures the exact brand, model, and physical state of your assets in real-time. A narrated video acts as a timestamped witness for the adjuster. This level of detail makes it much harder for insurance companies to apply generic depreciation to your claim.

Can I still claim items if I lost the original receipts in a fire?

You can still recover your losses without receipts by providing secondary evidence of ownership. Adjusters accept high-quality video footage, photos of serial number plates, or digital copies of owner’s manuals. This is why a digital household items list for insurance claims is your best defense. If you have video proof from SnapGuard, you have established ownership regardless of missing paperwork.

How much detail do I really need for low-value items like clothes?

You don’t need to list every individual item; instead, you should document by category and volume. Record “15 pairs of designer jeans” or “20 linear feet of hanging professional attire” to establish a baseline quality. This allows the adjuster to calculate a bulk value. For high-end fashion, always capture the brand label on camera to ensure you receive a “like-kind” replacement payout.

What happens if I forget to list an item on my initial insurance claim?

You can usually amend your claim by filing a supplemental list, but this often delays your final payout. Most policies allow for these updates for up to one or two years depending on your specific contract. However, proving an item existed months after the debris is cleared is notoriously difficult. Proactive documentation with SecureGuard prevents these costly omissions from the very beginning.

Does my home insurance policy cover the full replacement cost of all items?

It depends entirely on whether you have a Replacement Cost Value (RCV) or Actual Cash Value (ACV) policy. Many standard policies default to ACV, which subtracts depreciation based on the age of the item. If a 5-year-old laptop is destroyed, ACV pays its current used value, while RCV pays for a brand-new equivalent. Review your declarations page to confirm you have the coverage you expect.

How often should I update my household items list?

Update your inventory at least once a year or immediately after any major purchase. Most families add between $2,000 and $5,000 in new assets annually through holiday gifts and home upgrades. Scheduling a “Documentation Day” every January ensures your household items list for insurance claims remains current. Use HomeGuard to quickly record new items as they enter your home to keep your defense airtight.

What are the most common items adjusters reject due to lack of proof?

Adjusters frequently reject claims for high-end electronics, jewelry, and designer handbags without specific proof of brand and model. If you claim a “pro-grade camera” but only show a blurry photo of a black box, they will pay for a base-level model. Capturing serial numbers and brand logos is the only way to secure the full value of these premium assets during a total loss.

Is it worth documenting items in my storage unit or garage?

Yes; these items are typically covered under your primary homeowners policy, often up to a 10% limit of your personal property coverage. Garages contain expensive tools, lawn equipment, and seasonal gear that can easily total over $10,000. Use ClaimGuard strategies to ensure these off-site or exterior assets are included in your recovery plan before a disaster strikes.